The Economist explains its research from March 2013 -- Keep reading!

Language study

Johnson: What is a foreign language worth?

JOHNSON is a fan of the Freakonomics books and columns. But this week’s podcastmakes me wonder if the team of Stephen Dubner and Steven Levitt aren’t overstretching themselves a bit. “Is learning a foreign language really worth it?”, asks the headline. A reader writes:

My oldest daughter is a college freshman, and not only have I paid for her to study Spanish for the last four or more years — they even do it in grade school now! — but her college is requiring her to study EVEN MORE! What on earth is going on? How did it ever get this far? … Or to put it in economics terms, where is the ROI?

To sum up the podcast’s answers, there are pros and cons to language-learning. The pros are that working in a foreign language can make people make better decisions (research Johnson covered here) and that bilingualism helps with executive function in children and dementia in older people (covered here). The cons: one study finds that the earnings bonus for an American who learns a foreign language is just 2%. If you make $30,000 a year, sniffs Mr Dubner, that’s just $600.

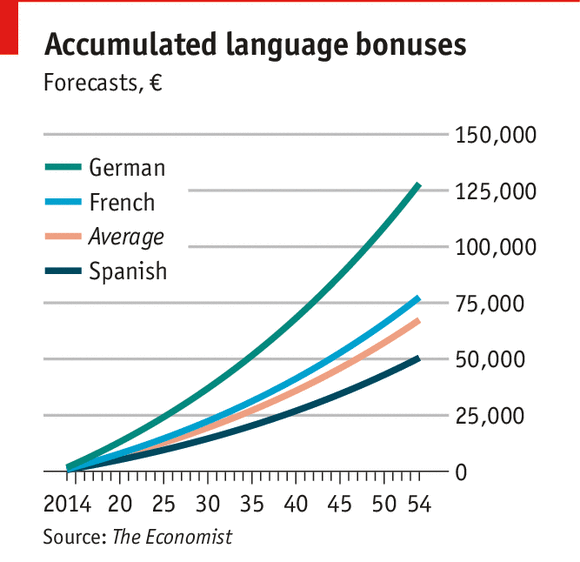

But for the sake of provocation, Mr Dubner seems to have low-balled this. He should know the power of lifetime earnings and compound interest. First, instead of $30,000, assume a university graduate, who in America is likelier to use a foreign language than someone without university. The average starting salary is almost $45,000. Imagine that our graduate saves her “language bonus”. Compound interest is the most powerful force in the universe (a statement dubiously attributed to Einstein, but nonetheless worth committing to memory). Assuming just a 1% real salary increase per year and a 2% average real return over 40 years, a 2% language bonus turns into an extra $67,000 (at 2014 value) in your retirement account. Not bad for a few years of “où est la plume de ma tante?”

Second, Albert Saiz, the MIT economist whocalculated the 2% premium, found quite different premiums for different languages: just 1.5% for Spanish, 2.3% for French and 3.8% for German. This translates into big differences in the language account: your Spanish is worth $51,000, but French, $77,000, and German, $128,000. Humans are famously bad at weighting the future against the present, but if you dangled even a post-dated $128,000 cheque in front of the average 14-year-old, Goethe and Schiller would be hotter than Facebook.

Why do the languages offer such different returns?

It has nothing to do with the inherent qualities of Spanish, of course. The obvious answer is the interplay of supply and demand.This chart reckons that Spanish-speakers account for a bit more of world GDP than German-speakers do. But an important factor is economic openness. Germany is a trade powerhouse, so its language will be more economically valuable for an outsider than the language of a relatively more closed economy.

But in American context (the one Mr Saiz studied), the more important factor is probably supply, not demand, of speakers of a given language. Non-Latino Americans might study Spanish because they hear and see so much of it spoken in their country. But that might be the best reason not to study the language, from a purely economic point of view. A non-native learner of Spanish will have a hard time competing with a fluent native bilingual for a job requiring both languages. Indeed, Mr Saiz found worse returns for Spanish study in states with a larger share of Hispanics. Better to learn a language in high demand, but short supply—one reason, no doubt, ambitious American parents are steering their children towards Mandarin. The drop-off in recent years in the American study of German might be another reason for young people to hit the Bücher.

And studies like Mr Saiz’s can only work with the economy the researchers have at hand to study. But of course changes in educational structures can have dynamic effects on entire economies. A list of the richest countries in the world is dominated by open, trade-driven economies. Oil economies aside, the top ten includes countries where trilingualism is typical, like Luxembourg, Switzerland and Singapore, and small countries like the Scandinavian ones, where English knowledge is excellent.

There are of course many reasons that such countries are rich. But a willingness to learn about export markets, and their languages, is a plausible candidate. One study, led byJames Foreman-Peck of Cardiff Business School, has estimated that lack of foreign-language proficiency in Britain costs the economy £48 billion ($80 billion), or 3.5% of GDP, each year. Even if that number is high, the cost of assuming that foreign customers will learn your language, and never bothering to learn theirs, is certainly a lot greater than zero. So...of course greater investment in foreign-language teaching would have other dynamic effects: more and better teachers and materials, plus a cultural premium on multilingualism, means more people will actually master a language, rather than wasting several years never getting past la plume de ma tante, as happens in Britain and America.

To be sure, everything has an opportunity cost. An hour spent learning French is an hour spent not learning something else. But it isn’t hard to think of school subjects that provide less return—economically, anyway—than a foreign language. What is the return on investment for history, literature or art? Of course schools are intended to do more than create little GDP-producing machines. (And there are also great non-economic benefits to learning a foreign language.) But if it is GDP you’re after, the world isn’t learning English as fast as some people think. One optimistic estimate is that half the world’s people might speak English by 2050. That leaves billions who will not, and billions of others who remain happier (and more willing to spend money) in their own language.

No comments:

Post a Comment