Saturday, April 30, 2016

What is a foreign language worth?

The Economist explains its research from March 2013 -- Keep reading!

Language study

Johnson: What is a foreign language worth?

JOHNSON is a fan of the Freakonomics books and columns. But this week’s podcastmakes me wonder if the team of Stephen Dubner and Steven Levitt aren’t overstretching themselves a bit. “Is learning a foreign language really worth it?”, asks the headline. A reader writes:

My oldest daughter is a college freshman, and not only have I paid for her to study Spanish for the last four or more years — they even do it in grade school now! — but her college is requiring her to study EVEN MORE! What on earth is going on? How did it ever get this far? … Or to put it in economics terms, where is the ROI?

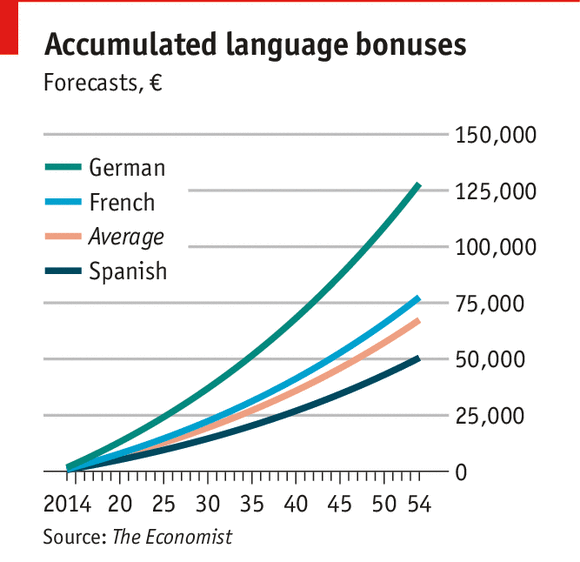

To sum up the podcast’s answers, there are pros and cons to language-learning. The pros are that working in a foreign language can make people make better decisions (research Johnson covered here) and that bilingualism helps with executive function in children and dementia in older people (covered here). The cons: one study finds that the earnings bonus for an American who learns a foreign language is just 2%. If you make $30,000 a year, sniffs Mr Dubner, that’s just $600.

But for the sake of provocation, Mr Dubner seems to have low-balled this. He should know the power of lifetime earnings and compound interest. First, instead of $30,000, assume a university graduate, who in America is likelier to use a foreign language than someone without university. The average starting salary is almost $45,000. Imagine that our graduate saves her “language bonus”. Compound interest is the most powerful force in the universe (a statement dubiously attributed to Einstein, but nonetheless worth committing to memory). Assuming just a 1% real salary increase per year and a 2% average real return over 40 years, a 2% language bonus turns into an extra $67,000 (at 2014 value) in your retirement account. Not bad for a few years of “où est la plume de ma tante?”

Second, Albert Saiz, the MIT economist whocalculated the 2% premium, found quite different premiums for different languages: just 1.5% for Spanish, 2.3% for French and 3.8% for German. This translates into big differences in the language account: your Spanish is worth $51,000, but French, $77,000, and German, $128,000. Humans are famously bad at weighting the future against the present, but if you dangled even a post-dated $128,000 cheque in front of the average 14-year-old, Goethe and Schiller would be hotter than Facebook.

Why do the languages offer such different returns?

It has nothing to do with the inherent qualities of Spanish, of course. The obvious answer is the interplay of supply and demand.This chart reckons that Spanish-speakers account for a bit more of world GDP than German-speakers do. But an important factor is economic openness. Germany is a trade powerhouse, so its language will be more economically valuable for an outsider than the language of a relatively more closed economy.

But in American context (the one Mr Saiz studied), the more important factor is probably supply, not demand, of speakers of a given language. Non-Latino Americans might study Spanish because they hear and see so much of it spoken in their country. But that might be the best reason not to study the language, from a purely economic point of view. A non-native learner of Spanish will have a hard time competing with a fluent native bilingual for a job requiring both languages. Indeed, Mr Saiz found worse returns for Spanish study in states with a larger share of Hispanics. Better to learn a language in high demand, but short supply—one reason, no doubt, ambitious American parents are steering their children towards Mandarin. The drop-off in recent years in the American study of German might be another reason for young people to hit the Bücher.

And studies like Mr Saiz’s can only work with the economy the researchers have at hand to study. But of course changes in educational structures can have dynamic effects on entire economies. A list of the richest countries in the world is dominated by open, trade-driven economies. Oil economies aside, the top ten includes countries where trilingualism is typical, like Luxembourg, Switzerland and Singapore, and small countries like the Scandinavian ones, where English knowledge is excellent.

There are of course many reasons that such countries are rich. But a willingness to learn about export markets, and their languages, is a plausible candidate. One study, led byJames Foreman-Peck of Cardiff Business School, has estimated that lack of foreign-language proficiency in Britain costs the economy £48 billion ($80 billion), or 3.5% of GDP, each year. Even if that number is high, the cost of assuming that foreign customers will learn your language, and never bothering to learn theirs, is certainly a lot greater than zero. So...of course greater investment in foreign-language teaching would have other dynamic effects: more and better teachers and materials, plus a cultural premium on multilingualism, means more people will actually master a language, rather than wasting several years never getting past la plume de ma tante, as happens in Britain and America.

To be sure, everything has an opportunity cost. An hour spent learning French is an hour spent not learning something else. But it isn’t hard to think of school subjects that provide less return—economically, anyway—than a foreign language. What is the return on investment for history, literature or art? Of course schools are intended to do more than create little GDP-producing machines. (And there are also great non-economic benefits to learning a foreign language.) But if it is GDP you’re after, the world isn’t learning English as fast as some people think. One optimistic estimate is that half the world’s people might speak English by 2050. That leaves billions who will not, and billions of others who remain happier (and more willing to spend money) in their own language.

Wednesday, April 27, 2016

Amnesty Int'l: Sei Dabei: Dein Boot fuer die Fluechtlinge

"315" src="https://www.youtube.com/embed/has_hdbrPIY" frameborder="0" allowfullscreen>

Verstanden?

Bis wann sollten die Boote alle gebaut und gesammelt werden?

Ist das Problem jetzt geloesst?

Verstanden?

Bis wann sollten die Boote alle gebaut und gesammelt werden?

Ist das Problem jetzt geloesst?

Tuesday, April 26, 2016

Je...Desto: German is EASY!

Word of the Day – “Je… desto…”

Hello everyone, and welcome to our German Word of the Day, and today it is time for a

TAG-TEAM-SPECIAL

This time we will look at the meaning and the grammar of:

“je … desto” (pron.: yeh dasto)

Suppose you want to express how some ‘quantity’ depends on some other ‘quantity’. In English, there is one word that will do the job for you… the .

- The more I study, the wiser I become.

- The longer I think about it, the less I want to see this movie.

- The bigger the better.

In German, one word is not enough to do this. You need a team: je… desto . Je itself has several meanings. It can mean ‘a‘ in sense of ‘per’ as in.

- Die Äpfel kosten 10 Euro je Kilo.

- The apples are 10 Euro a kilo.

Wow, some expensive apples.

Je can also mean ever. But ONLY in sense of ‘once at all’…. so it’s not a universal translation for ever.

Je can also mean ever. But ONLY in sense of ‘once at all’…. so it’s not a universal translation for ever.

- Has grammar ever been fun?

- Hat Grammatik je/jemals Spaß gemacht?

Cool.

Desto by itself does not have a meaning. You will only see it in combination with je to express the the-the-relation. [I just bit my tongue by the way.] Time for examples.

Desto by itself does not have a meaning. You will only see it in combination with je to express the the-the-relation. [I just bit my tongue by the way.] Time for examples.

- The more I study, the wiser I become.

- Je mehr ich studiere, desto weiser werde ich.

- The more I sleep the more tired I am.

- Je mehr ich schlafe, desto müder bin ich.

So that was our look at the very very hyper useful combination je… desto… and you definitely should learn and use it.

COMMENTS:

Here are some sentences for you to try right now!

COMMENTS:

Nice post! Just to clarify, so after “desto” comes the adjective, then the verb and then finally the pronoun?

- Genau :). It’s like a regular standard sentence with a desto in front of it.

jacbop

Ich finde diese Wortstellung verwirrend. Sie ist ähnlich wie “wenn/dann”, nicht wahr?Ich erwarte das Verb in der zweiten Position, zu stehen. Ich werde noch einmal die Beiträge über Wortstellung lesen, die Wortstellung dieser folgenden Sätze mich wirklich verwirrt.Je mehr ich lerne, desto mehr Ausnahmen finde ich.

Wenn ich das wüsste, dann wäre ich zufrieden.

Ich denke, dieses Satz ist blöd.

Ich glaube, diese Satz ist ohne ‘dass’ ein bisschen verwirrend.Keine von dieser Sätze haben das Verb im zweiten Position. Kannst du mir mir helfen, es besser zu verstehen?Danke sehr!- Gute Fragen :)… aber alle Sätze haben das Verb in Position 2.Also … die Struktur von “je… desto” ist wirklich merkwürdig. Man muss es glaube ich als wie-Box interpretieren.– [Langsam] lese ich

– I read [slowly].– [ Je müder ich bin, desto langsamer] lese ich.

– (no English translation that would mirror the structure)Für diese Interpretation spricht auch, dass man mit dem “je… desto” Teil alleine auf eine wie-Frage antworten kann– “Wie lange bleibst du in Berlin

“Je länger desto besser.”Im Grunde haben wir also ein Box und dann das Verb und alles ist normal :)“Wenn…, dann”Das “dann” ist einfach eine Dopplung und dient vor allem der Betonung.– If I knew that, [then] I would be happy.Solche Dopplungen findet man auch mit “da” manchmal– [Gestern auf dem Markt – wo-Box], [da wo-Box gedoppelt] habe ich mir Gemüse gekauft.“Ich denke,…”Bei Verben wie “denken, sagen, wissen, glauben” und kurzen Statements wird oft die Hauptsatzstruktur verwendet.

Also:– Ich denke, dieser Satz ist blöd.anstatt:– Ich denke, dass dieser Satz blöd ist.Es ist quasi wie direkte Rede:– Ich denke: “Dieser Satz ist blöd.”

– Ich glaube: “Dieser Satz ist ohne ‘dass’ ein bisschen verwirrend.In diesen Konstruktionen haben beide Sätze ihr Verb auf Platz 2– Ich (1) denke (2) manchmal (3), ich (1) sollte (2) mal die Küche sauber machen.

Hoffe, das hilft

(das war ein Beispiel, wo das Verb auf 1 ist… das “ich” habe ich einfach weggelassen :)- Danke sehr für die Erklärung!

Kurz gesagt:

– ‘je.., desto’: als eine große wie-Box

– ‘wenn…, dann’: ‘dann’ ist eine Dopplung wie ‘da’ und verbraucht keine Position

– ‘denken’, ‘glauben’, ‘meinen’: wie direkt Rede mit dem Doppelpunkt

Sehr hilfreich!

Here are some sentences for you to try right now!

- The more money I spend, the less I save. _______________________________________________

- The more wars we fight, the less safe I feel. _______________________________________________

- It seems to me that the nicer I am, the fewer friends I have. _____________________________

- I know that the more we dance, the better we’ll get. __________________________________________

- The longer he practices, the more he understands. ___________________________________________

- The more attentively you drive, the safer you'll be. ___________________________________________

Friday, April 22, 2016

Step Into German : 10 Contest Finalists

VOTE: Who should travel to Germany and meet Joris?

WHOA: 3 of the finalists are from Fayetteville-Manlius High School, Manlius, New York.

[Do you remember this school? We've seen several of their truly outstanding 1-take music videos.]

WHOA: 3 of the finalists are from Fayetteville-Manlius High School, Manlius, New York.

[Do you remember this school? We've seen several of their truly outstanding 1-take music videos.]

FINAL SELECTION : best to use the VOTE link above.

Adam Riegler, Staples High School, Westport, Connecticut  Watch the video & vote! Watch the video & vote!

|

Caroline Townsend et al., Lawrence North High School, Indianapolis, Indiana Watch the video & vote! |

Matt Dai et al., Fayetteville-Manlius High School, Manlius, New York Watch the video & vote! |

Emma Gardner, Vergennes Union High School, Vergennes, Vermont Watch the video & vote!

|

Becket Gourlay and Carly Storro, Conval High School, Peterborough, New Hampshire Watch the video & vote! |

Michael Zrzavy et al., Conval High School, Peterborough, New Hampshire Watch the video & vote! |

Lucy Langenberg et al., Fayetteville-Manlius High School, Manlius, New York Watch the video & vote!

|

Sameen Shaikh &: Fiona Hoye, Fayetteville-Manlius High School, Manlius, New York Watch the video & vote! |

Emma Schaefer & Ava Lowell, Shining Mountain Waldorf School, Boulder, Colorado Watch the video & vote! |

Brenda Paulina and García Estrada, Preparatoria de Jalisco, Guadalajara, Jalisco (Mexico) Watch the video & vote! |

Monday, April 18, 2016

Christian Pulisic aus Hershey PA schießt ein Tor für BVB Dortmund!

Sonntag, den 18. April 2016

Nur Stuttgarts Timo Werner, der Ex-Schalker und Weltmeister Julian Draxler, sowie Teamkollege Nuri Sahin waren beim Debüt-Treffer noch jünger.

Der amerikanische Nationalspieler ist der zwölfte 17-jährige, der in der Bundesliga ein Tor erzielen konnte.

Wir müssen uns diesen Spieler merken, nicht wahr?

Nur Stuttgarts Timo Werner, der Ex-Schalker und Weltmeister Julian Draxler, sowie Teamkollege Nuri Sahin waren beim Debüt-Treffer noch jünger.

Der amerikanische Nationalspieler ist der zwölfte 17-jährige, der in der Bundesliga ein Tor erzielen konnte.

Wir müssen uns diesen Spieler merken, nicht wahr?

Der Rattenfänger von Hameln - zum Lesen; zum Zuhören

Der Rattenfänger von Hameln

Vor langer Zeit herrschte in der Stadt Hameln eine fürchterliche Ratten- und Mäuseplage. Alles, was den Tieren in die Quere kam, wurde angenagt und aufgefressen.Da waren Hamelns Bürger und allen voran der Bürgermeister sehr froh, als eines Tages ein Mann in die Stadt kam, der versprach, Hameln von dieser Plage zu befreien. Der Mann trug den Namen Bundting, weil er so bunte Kleidung trug, die jedermann sogleich ins Auge stach.

Natürlich wollte der Mann seinen Dienst nicht umsonst verrichten, aber schnell war man sich über einen Geldbetrag einig. Den sollte Bundting erhalten, wenn alle Mäuse und Ratten aus der Stadt entfernt worden seien.

Und so geschah es auch. Kaum war der Vertrag zwischen dem Bürgermeister und dem Rattenfänger, so nannte sich der Mann, geschlossen, da nahm er aus seiner Jackentasche eine kleine Flöte und spielte darauf eine wunderschöne Melodie. Kaum aber hatte er den ersten Ton angeschlagen, da kamen schon aus allen Ecken und Winkeln die Ratten und Mäuse gelaufen und schlossen sich dem Rattenfänger an.

Als er nun meinte, alle Tiere eingesammelt zu haben, da zog er mit ihnen aus dem Stadttor hinaus, ging an die Ufer der Weser, die durch Hameln fließt, und zog sich seine bunten Kleider aus. Dann stieg er hinab in den Fluss – und alle Ratten und Mäuse folgten ihm und ertranken in den Fluten.

Nun kehrte der Rattenfänger zurück in die Stadt, um seinen Lohn abzuholen. Doch den wollte man dem Herrn Bundting plötzlich nicht mehr zahlen und so musste er unverrichteter Dinge abziehen.

Einige Wochen später aber kehrte der Rattenfänger zurück nach Hameln. Dieses Mal kam er im Gewand eines Jägers daher, so dass ihn die Menschen nicht sofort erkannten. Wieder zog er seine kleine Flöte aus der Jackentasche und spielte jene wunderschöne Melodie, mit der er schon die Nagetiere aus Hameln gelockt hatte. Aber was war das! Dem Jäger mit seiner Flöte folgten dieses Mal nicht Ratten und Mäuse, sondern Mädchen und Jungen.

In Scharen liefen alle Kinder mit, die älter als vier Jahre waren.

Der Rattenfänger führte sie aus der Stadt hinaus, hin zu einem Berg, der Poppenberg genannt wird, wo er mit ihnen für immer verschwand, noch ehe jemand etwas davon bemerkt hatte.

Nur zwei Kinder, die sich etwas verspätet hatten, konnten dem Rattenfänger entkommen. Doch das eine Kind blieb nach dem Vorfall blind, so dass es den Weg nicht mehr zeigen konnte, und das andere wurde taubstumm, so dass es nichts mehr von den Geschehnissen berichten konnte.

Nur ein Kindermädchen hatte den Auszug der Mädchen und Jungen aus der Stadt beobachtet und später allen davon berichten können. Mütter und Väter, Großeltern, Tanten und Onkel trauerten sehr um ihre verlorenen Kinder.

Lange Zeit hieß in Hameln jene Straße, durch die die Kinder mit dem Rattenfänger gezogen waren, „bungelose“ Straße (stille, tonlose, trommellose Straße). Und selbst, wenn eine junge Braut an ihrem Hochzeitstage durch diese Straße zog, durfte dort niemals Musik gespielt werden.

MEHR ÜBER DIE STADT HAMMELN IST HIER.

Fraktur - Gespenstliteratur

HIER KANN MANN IM INTERNET IN FRAKTUR LESEN

Dank Fluent U, as it explores Halloween topics (see Wortschatz):

A master marksman finds himself unable to catch any wild swine or deer in the dark autumn forests. One day, he’s approached by a mysterious peddler wrapped in a cloak that conceals his face. The peddler offers the marksman seven bullets, with one condition. The first six bullets will hit whatever the marksman wants them to hit, but the peddler will choose the trajectory of the seventh. The marksman agrees.

The marksman quickly earns himself a reputation as the best hunter in the village, as he brings home wild boar after wild boar. He catches the eye of the prettiest girl in town, and they fall in love.

But all too soon, the marksman uses up all six bullets, and when he shoots the seventh, it goes astray and hits his love in the chest, killing her.

The peddler appears to the distraught marksman and reveals himself as the devil. Live a pious life, repent of your hubris, and you will be reunited with the girl after your death, the devil tells the marksman. The marksman tries, but he is overcome by desire for another girl in the village, and he marries her instead.

One year to the day after his bullet pierced his original love’s chest, he is riding in the forest when he comes across a clearing where skeletons dance around cold flames. One of the skeletons, the girl’s, waltzes with him all night, and the next morning, the villagers find the marksman and his horse, dead, at the edge of the forest.

What’s the backstory?

Folktales about Freischütze were common in the 1500s, 1600s and 1700s in Germany. The tale was first written down in “Das Gespensterbuch” (The Ghost Book), a collection of German ghost and folk stories compiled in the 1810s and published in five volumes. The story subsequently became the inspiration for an opera by Carl Maria von Weber.

Are you tempted to open the link above and ready this story? Reading in Fraktur has become all but a lost skill. [But it's completely decipherable with time.] -rsb

Learn these 20 spooky vocabulary words, and you’ll be telling ghost stories in German in no time.

Dank Fluent U, as it explores Halloween topics (see Wortschatz):

Der Freischütz (The Marksman)

What’s the story?A master marksman finds himself unable to catch any wild swine or deer in the dark autumn forests. One day, he’s approached by a mysterious peddler wrapped in a cloak that conceals his face. The peddler offers the marksman seven bullets, with one condition. The first six bullets will hit whatever the marksman wants them to hit, but the peddler will choose the trajectory of the seventh. The marksman agrees.

The marksman quickly earns himself a reputation as the best hunter in the village, as he brings home wild boar after wild boar. He catches the eye of the prettiest girl in town, and they fall in love.

But all too soon, the marksman uses up all six bullets, and when he shoots the seventh, it goes astray and hits his love in the chest, killing her.

The peddler appears to the distraught marksman and reveals himself as the devil. Live a pious life, repent of your hubris, and you will be reunited with the girl after your death, the devil tells the marksman. The marksman tries, but he is overcome by desire for another girl in the village, and he marries her instead.

One year to the day after his bullet pierced his original love’s chest, he is riding in the forest when he comes across a clearing where skeletons dance around cold flames. One of the skeletons, the girl’s, waltzes with him all night, and the next morning, the villagers find the marksman and his horse, dead, at the edge of the forest.

What’s the backstory?

Folktales about Freischütze were common in the 1500s, 1600s and 1700s in Germany. The tale was first written down in “Das Gespensterbuch” (The Ghost Book), a collection of German ghost and folk stories compiled in the 1810s and published in five volumes. The story subsequently became the inspiration for an opera by Carl Maria von Weber.

Are you tempted to open the link above and ready this story? Reading in Fraktur has become all but a lost skill. [But it's completely decipherable with time.] -rsb

Learn these 20 spooky vocabulary words, and you’ll be telling ghost stories in German in no time.

- der Geist (the ghost)

- die Gespenstergeschichte/Geistergeschichte (the ghost story)

- das Kostüm (the costume)

- das Gespensterhaus/Geisterhaus (the haunted house)

- der Vampir (the vampire)

- der Teufel (the devil)

- das Volksmärchen (the folktale)

- spuken (to haunt/spook)

- das Zauberwald (the haunted forest)

- gruselig/unheimlich (spooky)

- die Hexe (the witch)

- der Fluch (the curse)

- der Friedhof (the cemetery)

- die Untoten (the undead)

- der Schadenzauber (black magic)

- das Geisterschloss (haunted castle)

- der Ghul (the ghoul)

- die Gruselgeschichte (the scary story)

- das Monster (the monster)

- übernatürlich (supernatural)

Saturday, April 16, 2016

Berlin goes Gaza -- Zwischentöne

Robert Bosch Stiftung: Georg Eckert Institut - Leibniz-Institut für Internationals Schulbuchfroschung

THEMA: Der Nahostkonflikt löst auch in Deutschland immer wieder heftige Debatten aus. In Medienberichten wird in diesem Zusammenhang vor "importierten Konflikten" gewarnt, die durch die Spannungen im Nahen Osten unter Muslimen und Juden in Deutschland ausgelöst werden könnten. Aber auch nichtmuslimische und nichtjüdische Menschen verfolgen den die Ereignisse in Israel und Palästina mit besonderer Emotionalität.

45 Min. Film:

http://www.zwischentoene.info/themen/unterrichtseinheit/materialien/ue/berlin-goes-gaza.html#content

Projektgruppe "Salam Berlin Shalom" 2010

hentoene.info/themen/unterrichtseinheit/praesentation/ue/berlin-goes-gaza.html

Wir lernen über

Gelaal und Ahmed aus Palestinien

Joel, ein Jude in Berlin

Timur, ein Jude neulich Deutscher aus Weißrussland

Zitate aus dem Film:

Zitat 1 „Ich fühle mich als Moslem, aber auch ein bisschen als Deutscher – hat mit Moslem zwar nichts zu tun – und als Palästinenser und ich interessiere mich auch dafür.“

Zitat 2: „Wissen Sie, das ist komisch und wenn ich jetzt zum Beispiel hier bin und dann wenn ich zum Beispiel nach Marzahn gehe und sage: „Ey, ich bin Deutscher!“ – da glaubt mir nicht ein einziger. Wenn ich jetzt rübergehe in den Libanon gehe und dort sage: „Hey Freunde, ich bin Araber!“ – da glaubt mir auch nicht einer, da sagen sie: „Ey, du bist Deutscher, du bist kein Araber.““

Zitat 3 „Deine Leute haben meinen Onkel umgebracht.“ „Wie meine Leu kein Israeli.“ „Ja, du bist doch Jude.“ „Ja, aber das das ist die gleiche Religion, aber... Das finde ich furchtbar, wie manche Leute so verallgemeinern, dass echt viele der Meinung sind, dass Jude ist auch gleich Israeli. Nein! Jude ist Jude. Israeli ist israelischer Staatsbürger.“

Zitat 4 „Ich trenne das, gerade weil ich hier lebe in Deutschland. Für mich ist der Staat Israel Israel-Staat. Und äh – es gibt auch israelische Moslems. Es gibt auch israelische Palästinenser. Es spielt ja in dem Moment keine Rolle. Ich trenne das jüdisch, israelisch, palästinensisch, Moslem, Christ.“

ARBEITSBLATT

„WAS MACHT MICH AUS?“

Das macht mich aus:

________________________________________________________________

________________________________________________________________

________________________________________________________________

Diese Ereignisse haben mich geprägt oder sind mir wichtig

(zum Beispiel aus der Geschichte, Politik, Familie):

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

_____________________________________________________________

Rana Göroglu, "Was geht mich Palästina an?" Eine Reise nach Jerusalem, Newsletter Jugendkultur, Religion und politische Bildung, 18/Aug, 2010. (online) (Seite 7)

Seite 10: ,,Menschen ohne Religion verstehen das nicht!"

Hier von ZEIT ONLINE gibt es eine Fernsehsendung über Pakistan, die sich um Sexualität und Gesundheit handelt:

THEMA: Der Nahostkonflikt löst auch in Deutschland immer wieder heftige Debatten aus. In Medienberichten wird in diesem Zusammenhang vor "importierten Konflikten" gewarnt, die durch die Spannungen im Nahen Osten unter Muslimen und Juden in Deutschland ausgelöst werden könnten. Aber auch nichtmuslimische und nichtjüdische Menschen verfolgen den die Ereignisse in Israel und Palästina mit besonderer Emotionalität.

45 Min. Film:

http://www.zwischentoene.info/themen/unterrichtseinheit/materialien/ue/berlin-goes-gaza.html#content

Projektgruppe "Salam Berlin Shalom" 2010

hentoene.info/themen/unterrichtseinheit/praesentation/ue/berlin-goes-gaza.html

Wir lernen über

Gelaal und Ahmed aus Palestinien

Joel, ein Jude in Berlin

Timur, ein Jude neulich Deutscher aus Weißrussland

Zitate aus dem Film:

Zitat 1 „Ich fühle mich als Moslem, aber auch ein bisschen als Deutscher – hat mit Moslem zwar nichts zu tun – und als Palästinenser und ich interessiere mich auch dafür.“

Zitat 2: „Wissen Sie, das ist komisch und wenn ich jetzt zum Beispiel hier bin und dann wenn ich zum Beispiel nach Marzahn gehe und sage: „Ey, ich bin Deutscher!“ – da glaubt mir nicht ein einziger. Wenn ich jetzt rübergehe in den Libanon gehe und dort sage: „Hey Freunde, ich bin Araber!“ – da glaubt mir auch nicht einer, da sagen sie: „Ey, du bist Deutscher, du bist kein Araber.““

Zitat 3 „Deine Leute haben meinen Onkel umgebracht.“ „Wie meine Leu kein Israeli.“ „Ja, du bist doch Jude.“ „Ja, aber das das ist die gleiche Religion, aber... Das finde ich furchtbar, wie manche Leute so verallgemeinern, dass echt viele der Meinung sind, dass Jude ist auch gleich Israeli. Nein! Jude ist Jude. Israeli ist israelischer Staatsbürger.“

Zitat 4 „Ich trenne das, gerade weil ich hier lebe in Deutschland. Für mich ist der Staat Israel Israel-Staat. Und äh – es gibt auch israelische Moslems. Es gibt auch israelische Palästinenser. Es spielt ja in dem Moment keine Rolle. Ich trenne das jüdisch, israelisch, palästinensisch, Moslem, Christ.“

ARBEITSBLATT

„WAS MACHT MICH AUS?“

Das macht mich aus:

________________________________________________________________

________________________________________________________________

________________________________________________________________

Diese Ereignisse haben mich geprägt oder sind mir wichtig

(zum Beispiel aus der Geschichte, Politik, Familie):

________________________________________________________________

________________________________________________________________

________________________________________________________________

________________________________________________________________

_____________________________________________________________

Rana Göroglu, "Was geht mich Palästina an?" Eine Reise nach Jerusalem, Newsletter Jugendkultur, Religion und politische Bildung, 18/Aug, 2010. (online) (Seite 7)

Seite 10: ,,Menschen ohne Religion verstehen das nicht!"

Hier von ZEIT ONLINE gibt es eine Fernsehsendung über Pakistan, die sich um Sexualität und Gesundheit handelt:

(German Soccer League) DFB Integrationsspot

Wie sieht die wahre Deutsche Nationalmannschaft aus?

(Yes, the National Team is rather an integrated one, don't you agree?)

Wednesday, April 13, 2016

MWS: Die Zeitreisende Klassenzimmer

Hier sehen wir das Trojanischepferd von der Meadowbrook Waldorf Schule unterwegs nach NKHS!

Wer glaubt wir sollten wieder ein Theaterfest organizieren? Und diesmal mitspielen?

Oh-oh! Rammstein ist es nicht . . . .

ACHTUNG! Be Deutsch. [Germans on the rise!]

Die Welt dreht durch! Europa fühlt sich so schwach, dass es sich von 0,3% Flüchtlingen bedroht sieht, Amerika ist drauf und dran einen Mann zu wählen, bei dem niemand so genau weiß, wer unter dem Toupet die Fäden zieht und als wäre das alles noch nicht schlimm genug, muss man sich nun auch noch ausgerechnet von Deutschland darüber belehren lassen, wie man sich moralisch richtig verhält. Ausgerechnet Deutschland! Die haben noch nicht mal einen Weltkrieg gewonnen!

The world is going completely nuts!

Es gibt vieles drin, was ich normalerweise Euch nicht zeigen wuerde; was glaubt IHR? --rsb

NEO MAGAZIN ROYALE mit Jan Böhmermann - ZDFneo

Böhmermann persifliert im Rammstein-Look

die echten Deutschen#MakeGermanyGreatAgainbz-berlin.de/kultur/fernseh…

"We are proud of not being proud!"

[Achtung: Dieses Video ist vielleicht nicht fuer unser Klassenzimmer, aber es ist in Deutschland ein Viral-Hit geworden.]

die echten Deutschen#MakeGermanyGreatAgainbz-berlin.de/kultur/fernseh…

"We are proud of not being proud!"

[Achtung: Dieses Video ist vielleicht nicht fuer unser Klassenzimmer, aber es ist in Deutschland ein Viral-Hit geworden.]

Description: Mar 31, 2016

Die Welt dreht durch! Europa fühlt sich so schwach, dass es sich von 0,3% Flüchtlingen bedroht sieht, Amerika ist drauf und dran einen Mann zu wählen, bei dem niemand so genau weiß, wer unter dem Toupet die Fäden zieht und als wäre das alles noch nicht schlimm genug, muss man sich nun auch noch ausgerechnet von Deutschland darüber belehren lassen, wie man sich moralisch richtig verhält. Ausgerechnet Deutschland! Die haben noch nicht mal einen Weltkrieg gewonnen!

The world is going completely nuts!

Europe feels threatened by 0.3% refugees, the USA are about to elect a man, of whom no one really knows who is pulling the strings under the toupee, .

As if that was not bad enough, Germany of all nations has to advise the world as to how to behave morally right.

-- I mean GERMANY! They did not even win one single world war in history!

Es gibt vieles drin, was ich normalerweise Euch nicht zeigen wuerde; was glaubt IHR? --rsb

Monday, April 11, 2016

How to Make the Most of German Class to Attain Fluency

In our German class, your teacher does everything (= gives you lots of Comprehensible Input) for you to attain fluency in German as quickly and efficiently as possible.

But what are YOU expected to do in class? What strategies can you utilize to be the most efficient student possible in a class teaching the language with the aid of stories?

You are urged to observe…

Don’t take notes. Let the teacher do the writing.

Focus on the spoken word. The finer the ear you develop for the language, the better the speaker you’ll be.

Of course you will have to see what you hear. The teacher will write down every word and phrase used in the story. Notes and story text will be available online. You can also take snapshots of the teacher’s notes in class. (The ‘no note-taking’ rule is more relaxed with advanced students.)

Language you hear but don’t understand is nothing but noise. Your brain needs time to process and understand what you hear. The teacher will speak slowly and clearly because you have to understand everything he says. Believe it or not, this is the single prerequisite for you to develop 1) an ear for the language, and 2) the ability to speak it.

But what do you do if you don’t understand a word and get confused? Wait and try to figure it out on your own?

No. Here is what you do:

Stop the teacher. Right away. Ask him to clarify. Ask him to speak more slowly.

Unfortunately, despite his best efforts, the teacher always

tends to go too fast—with the result that you lose track. The teacher

may also use a word you’ve never heard and this, again, may confuse you.

Stop her every single time this happens. Stop her whenever she

goes too fast. Stop her whenever she uses a word you don’t understand. Do

this for your own sake and for your classmates’ sake.

You may think you do a disservice to your fellow students by slowing the class down but in fact you are doing a great service to everyone when you stop the teacher: the other students, even if they seem to be at a more advanced level, need more processing time just as well, and they’ll be happy to have a tiny little break. Clarifying the issue won’t last longer than a fraction of a minute!

When I ask a question and you know the answer, the challenge for you is to answer as fast and succinctly as possible. I want you to use the minimum possible number of words. I want a visceral answer, a gut answer, whenever possible—one that is felt, not premeditated. Please forget any ‘full sentence’ rule you may have heard in other courses. A single word to the point (or even just a gesture) is the best answer.

What’s even better than one word? No word! Nod or shake your head to say yes or no, point, gesture like mad, whatever it takes to convey what you think without words. The less you speak now, the sooner you’ll become a fluent speaker and the more you’ll sound like a native.

Your brain needs time to process what you hear. Focusing instead on what to say interferes with this and can be detrimental in language acquisition just as much as it is in a conversation.

Want to be a great conversationalist? Learn to listen well. Want to be a fluent speaker of Hungarian? Learn it by listening well.

Speaking little helps you achieve your goal of fluency in Hungarian. Speaking little or, in other words, increasing the amount of speech you produce only as you naturally become ready to speak more, has a number of benefits:

All in all, we want a story you find compelling. A memorable story. A story that’s fun and easy for you to recall. If the story sticks, the language will stick, too.

But what are YOU expected to do in class? What strategies can you utilize to be the most efficient student possible in a class teaching the language with the aid of stories?

You are urged to observe…

The Four Golden Rules of German Class

- Listen

- Understand

- Speak Little

- Be Wacky

RULE #1: LISTEN

Listen, listen, listen. Listen all the time.

The goal is for you to become fluent in Hungarian. To achieve this you’ll have to listen a hundred times more than you speak. (Just like young kids learning their first language.) Speaking is always a derivative of hearing.

Don’t take notes. Let the teacher do the writing.

Focus on the spoken word. The finer the ear you develop for the language, the better the speaker you’ll be.Of course you will have to see what you hear. The teacher will write down every word and phrase used in the story. Notes and story text will be available online. You can also take snapshots of the teacher’s notes in class. (The ‘no note-taking’ rule is more relaxed with advanced students.)

RULE #2: UNDERSTAND

Make sure you understand everything you hear.

The teacher will do his best to ensure you understand everything he says in Hungarian. He’ll write up and translate the new vocabulary for you and show how it’s used in context. He may ask the class to think of gestures which might in a way express the meaning. The class may spend a few minutes playing with gestures. (This fun activity is called TPR.) All this to establish meaning before starting on the story.Language you hear but don’t understand is nothing but noise. Your brain needs time to process and understand what you hear. The teacher will speak slowly and clearly because you have to understand everything he says. Believe it or not, this is the single prerequisite for you to develop 1) an ear for the language, and 2) the ability to speak it.

But what do you do if you don’t understand a word and get confused? Wait and try to figure it out on your own?

No. Here is what you do:

Stop the teacher. Right away. Ask him to clarify. Ask him to speak more slowly.

Unfortunately, despite his best efforts, the teacher always

tends to go too fast—with the result that you lose track. The teacher

may also use a word you’ve never heard and this, again, may confuse you.

Stop her every single time this happens. Stop her whenever she

goes too fast. Stop her whenever she uses a word you don’t understand. Do

this for your own sake and for your classmates’ sake.You may think you do a disservice to your fellow students by slowing the class down but in fact you are doing a great service to everyone when you stop the teacher: the other students, even if they seem to be at a more advanced level, need more processing time just as well, and they’ll be happy to have a tiny little break. Clarifying the issue won’t last longer than a fraction of a minute!

RULE #3: SPEAK LITTLE

Speak as little as you can get away with.

Take your time. Never for a moment struggle to speak. Don’t force it. Your brain needs time to process all the language you hear in class. Focus on listening. The time will come when words fall out of your mouth without you thinking.If you can answer the question with one word, don’t use two.

Short answers are used a lot in natural conversation and the art of using them is easy to master.When I ask a question and you know the answer, the challenge for you is to answer as fast and succinctly as possible. I want you to use the minimum possible number of words. I want a visceral answer, a gut answer, whenever possible—one that is felt, not premeditated. Please forget any ‘full sentence’ rule you may have heard in other courses. A single word to the point (or even just a gesture) is the best answer.

What’s even better than one word? No word! Nod or shake your head to say yes or no, point, gesture like mad, whatever it takes to convey what you think without words. The less you speak now, the sooner you’ll become a fluent speaker and the more you’ll sound like a native.

Your brain needs time to process what you hear. Focusing instead on what to say interferes with this and can be detrimental in language acquisition just as much as it is in a conversation.

Want to be a great conversationalist? Learn to listen well. Want to be a fluent speaker of Hungarian? Learn it by listening well.

Speaking little helps you achieve your goal of fluency in Hungarian. Speaking little or, in other words, increasing the amount of speech you produce only as you naturally become ready to speak more, has a number of benefits:

- It requires less effort (if any). Less effort = lower stress. Lower stress = more efficient learning.

- It makes you a better communicator. This is the way to go to communicate fast and smoothly.

- This way you also sound more natural, more like a native.

- Using just the one word needed (= the right word at the right time) helps you acquire a feel for stress—not the wrong kind of stress that makes you suffer but emphasis, the most important ingredient to comprehensible speech.

RULE #4: BE WACKY

Contribute surprising details to the story.

We either go to sleep or have a fun time in class. The last thing we want is a story that bores you. If everything is normal, nothing deserves attention. Feel free to be wacky when the teacher asks for a detail. If someone wants a pet, why shouldn’t it be a huge purple ant with green sunglasses and a red Ferrari or anything? Wackiness attracts attention. You’ll find it easier to retell the story with surprising detail.Contribute fun names to the story.

When asked for a name, throw in the name of a famous person or someone you know. Names that are easy to understand will help make the story more comprehensible.All in all, we want a story you find compelling. A memorable story. A story that’s fun and easy for you to recall. If the story sticks, the language will stick, too.

Why not give it a try?

The above rules apply to group sessions and one on one sessions alike, whether face to face or on Skype.

Subscribe to:

Posts (Atom)